Last November, ahead of the quarterly wave of 13F filings in the United States, we took a look at the Goldman Sachs Hedge Industry VIP ETF, which tracks the GS Hedge Fund VIP Index, to see how it was performing versus a broader equity index.

It’s time to do it again. As a reminder for those who missed the original post, Goldman Sachs publishes its ‘Goldman Sachs Hedge Fund VIP Index’, which, according to the index methodology, “consists of fundamentally driven hedge fund managers’ “Very-Important-Positions,” which appear most frequently among their top 10 long equity holdings.” The ETF tracks this index.

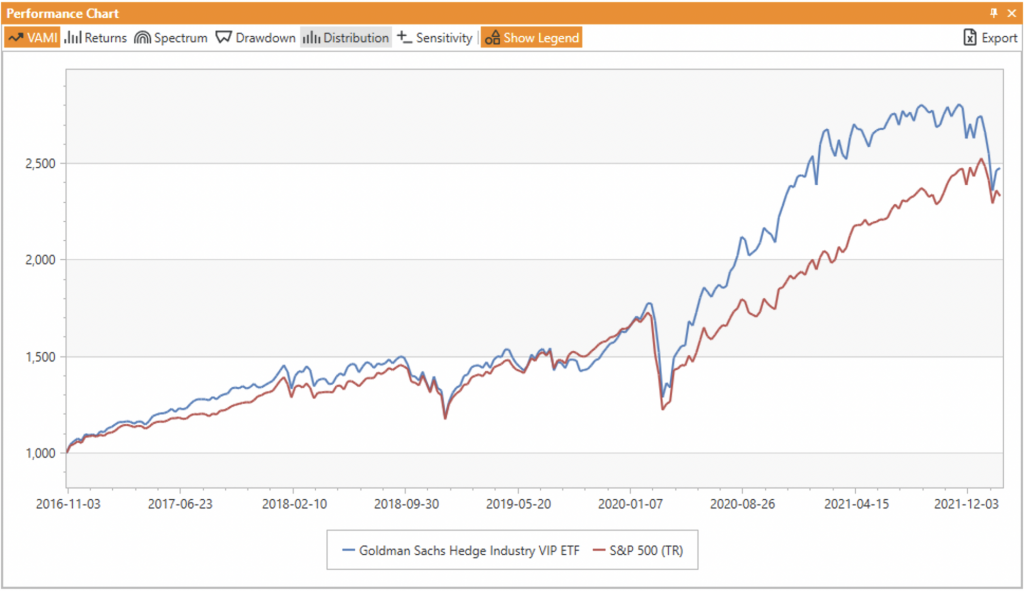

In November, we noted that the performance of the ETF appeared to be split into two distinct parts – prior to March 2020, when the world’s markets experienced a large and sudden drawdown at the outbreak of the COVID-19 pandemic and related lock-downs, and immediately after it.

Figure 1: GS Hedge Fund Industry VIP ETF vs. S&P 500, Nov 2016 to Feb 2022

Source: AlphaBot, GS, S&P

Prior to the drawdown, the ETF did not really do much different from the general market index. It was a little better at times, and sometimes a little worse, but those fluctuations basically washed each other out resulting in some steady oscillations around the general market. However, something changed going into April 2020 when the EFT literally exploded, and continued to outperform U.S. equities through mid-2021 (and that is on top of already strong equity market performance driven by global stimulus efforts). In the second half of 2021, the outperformance appeared to have exhausted itself, and the ETF’s performance reverted to something close to the mean.

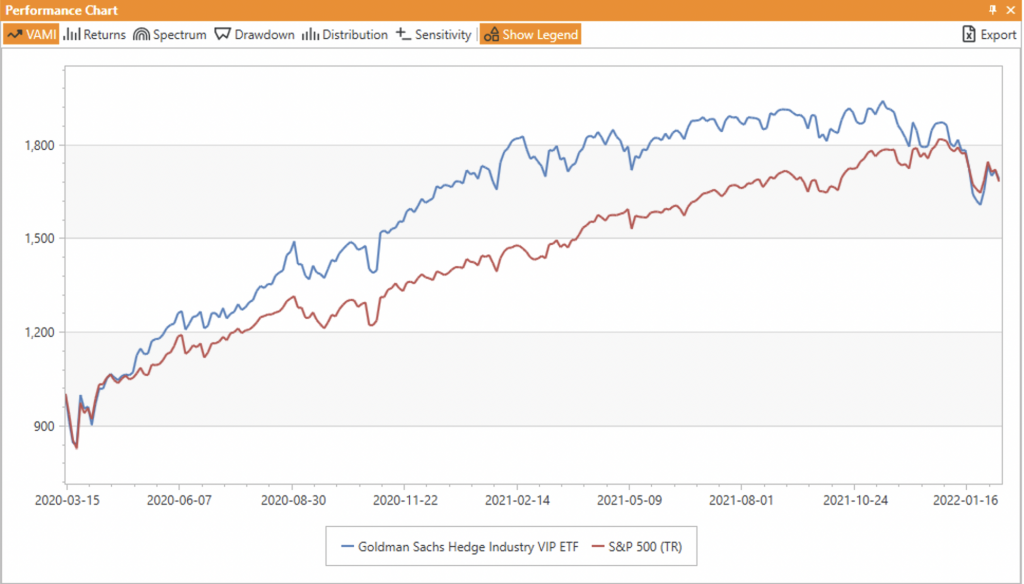

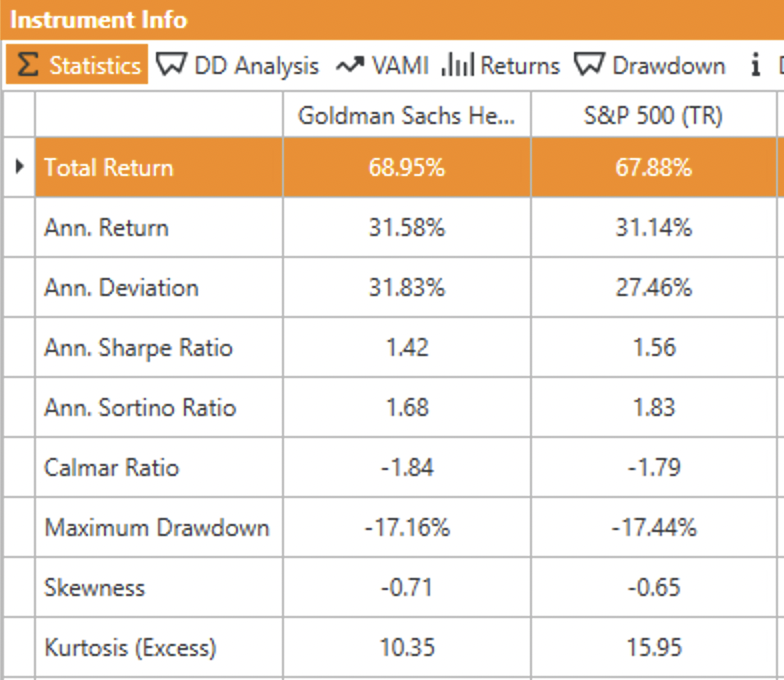

Has anything changed in the past three months? As of February 11, 2022, it appears that the outperformance of the past two years has completely reversed back to the performance of the broader market, with performance metrics for almost a year being nearly identical (figures 2 and 3 below). In fact, the S&P 500 shows better risk adjusted metrics because it did not suffer as much of a decline in January as the VIP set that got crushed pretty hard.

Figure 2 and 3: GS Hedge Fund Industry VIP ETF vs. S&P 500, March 2020 – February 2022

Source: AlphaBot, GS, S&P

I guess this is just more proof of the old “what goes up must come down” adage, as well as yet another case illustrating that market timing is both the most influential but difficult component to factor into one’s portfolio; missing entry and exit points by just a few weeks can completely change performance from outsized gains into outsized losses. Additionally, the data provides fuel for both those who believe that active management doesn’t outperform in the long term and those who think that hedge fund managers need to stay away from crowded trades in order to generate persistent alpha.

At the time of writing, we were expecting the new glut of 13F filings to be submitted to the SEC. We’ll revisit the Goldman Sachs Hedge Industry ETF in future to see if the hedge fund set can start beating the market again, as well as highlight some interesting portfolio construction techniques in our future posts, so stay tuned!